Page 7 - REPORT Brinkman 20-MAR Healthcare Roundtable

P. 7

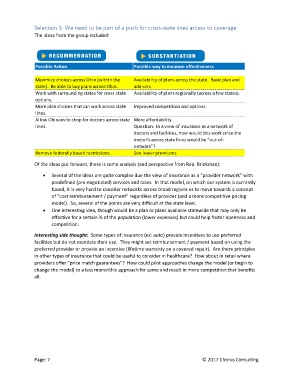

Selection 3: We need to be part of a push for cross-state lines access to coverage

The ideas from the group included:

Possible Action Possible way to measure effectiveness

Maximize choices across Ohio (within the Availability of plans across the state. Basic plan and

state). Be able to buy plans across Ohio. add-ons.

Work with surrounding states for cross-state Availability of plans regionally (across a few states).

options.

More plan choices that can work across state Improved competition and options.

lines.

Allow Ohioans to shop for doctors across state More affordability.

lines. Question: In a view of insurance as a network of

doctors and facilities, how would this work since the

doctor's across state lines would be "out-of-

network"?

Remove federally based restrictions. See lower premiums.

Of the ideas put forward, there is some analysis (and perspective from Rep. Brinkman):

• Several of the ideas are quite complex due the view of insurance as a “provider network” with

predefined (pre-negotiated) services and rates. In that model, on which our system is currently

based, it is very hard to consider networks across broad regions or to move towards a concept

of “cost reimbursement / payment” regardless of provider (and a more competitive pricing

model). So, several of the points are very difficult at the state level.

• One interesting idea, though would be a plan or plans available statewide that may only be

effective for a certain % of the population (lower expenses) but could help foster openness and

competition.

Interesting side thought: Some types of insurance (ex: auto) provide incentives to use preferred

facilities but do not mandate their use. They might set reimbursement / payment based on using the

preferred provider or provide an incentive (lifetime warranty on a covered repair). Are there principles

in other types of insurance that could be useful to consider in healthcare? How about in retail where

providers offer “price match guarantees”? How could pilot approaches change the model (or begin to

change the model) to a less monolithic approach for some and result in more competition that benefits

all.

Page: 7 © 2017 Chorus Consulting